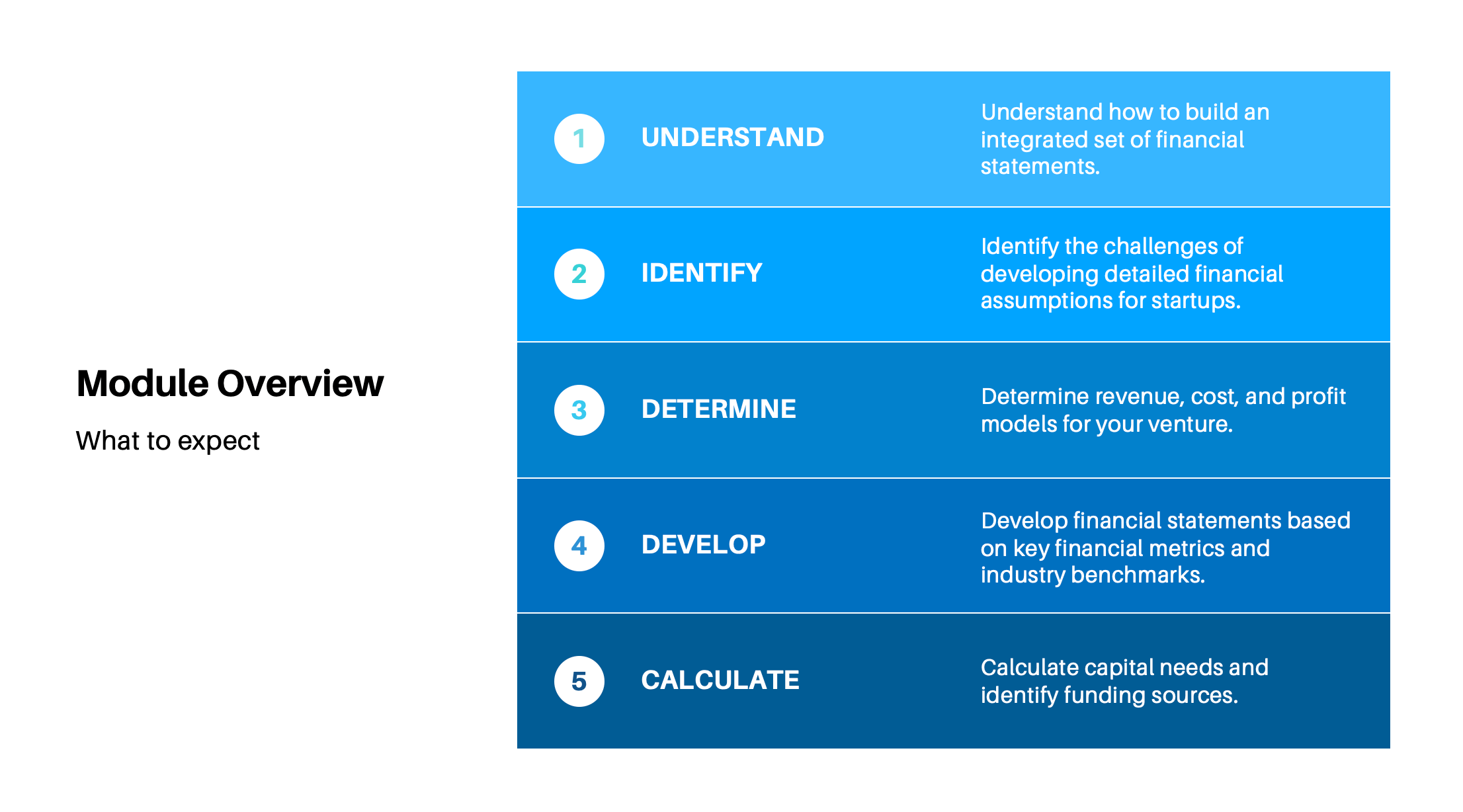

Module 7 | Your Financial Plan

Module Reading List: Selected Innovate and Thrive Posts

Module 7 Posts

Forecasting Financial Performance

A Financial Plan Is Not a Prediction

The Hidden Psychology of Cash Flow Disasters: How Smart Founders Sabotage Their Finances

A Guide to Building Reasonable Startup Financial Projections

Build Bulletproof Revenue Projections: An Integrated Modeling Approach for Startups

Determining Capital Requirements

Mastering Startup Financials: How to Determine Your Venture's Capital Needs

Harnessing Startup Financial Metrics: Key Insights for Sustainable Growth

The Pre-Launch Metrics Imperative: How Early Data Powers Startup Success and Reduces Risk

Identifying Funding Sources

Maximizing Startup Potential: Non-Equity Funding Strategies for Early-Stage Ventures

The Art of Self-Sufficiency: Unleashing Startup Potential through Bootstrapping

Nurture Your Startup's Potential: A Guide to Friends and Family Funding

Types of Crowdfunding: Choosing the Right Approach for Your Startup

Navigating Government Support Programs for Startups

Bridging Startup Runways: Inside Convertible Debt Instruments

Bridging Startups to Equity Capital: Incubators, Accelerators and Studios

Maximizing Startup Growth: Equity Funding Strategies for Later Stage Ventures

Do Angel Investors Still Matter Today?

Navigating the VC Landscape: A Comprehensive Guide